Accelerate Your Information Edge

Get ahead of the market with a research advantage driven by real-time indicators, unique views of multi-asset positioning, differentiated angles on macro strategy, advanced predictive analytics, and much more. Based on academic rigor, proprietary data, and deep expertise from across our Markets businesses, the Insights platform customizes the delivery of our full research suite to empower your investment team.

#1 FX#1

FX

FX

Bank for ResearchBank for

Research

Research

Again. For the third year in a row, State Street Markets has been named the #1 FX Bank for Research by Euromoney.

GET THE APP

Research on demand

Research on the go. Stay up to date with award-winning research and the latest in capital flows with our Insights mobile app.

What’s New

Market Signals and Shifts: What to watch in 2026

Our second annual State Street Markets outlook, Market signals and shifts: What to watch in 2026, examines the dominant forces shaping the year ahead through a lens that challenges consensus thinking.

Cross-Market Signals for the Summer

As markets enter vacation mode, this week's podcast presents our annual summer overview of the proprietary indicators available from State Street Markets and how they map to the most relevant themes driving assets and currencies. The sustainability of the tech trade in equities, the near-term path of inflation and the direction of travel for the Federal Reserve and how they feed into a rate, curve and FX view - it's all here. Host Tim Graf, Head of Macro Strategy for EMEA, talks through how unique ...

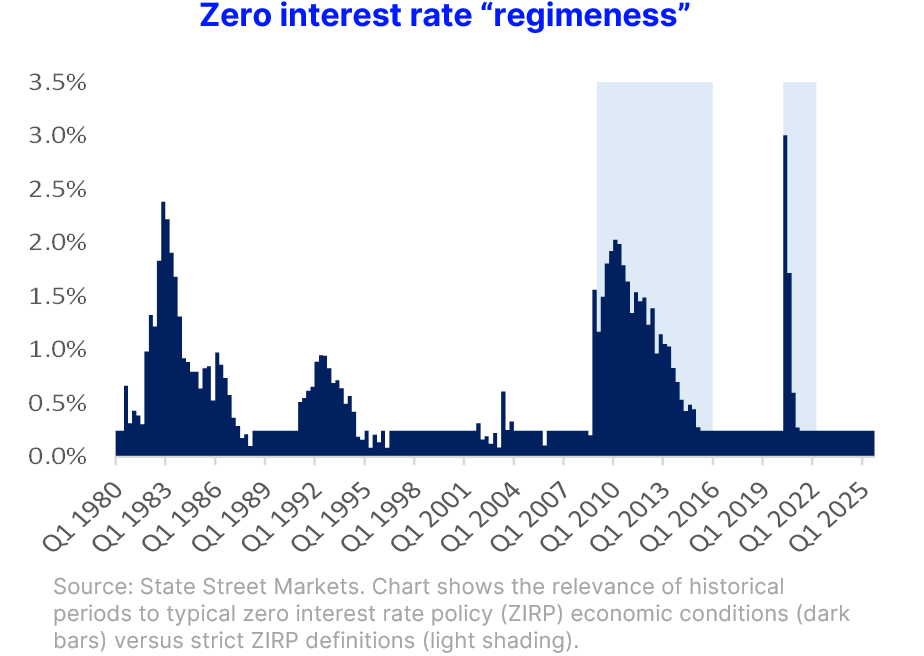

Policy Regimes versus Economic Regimes

Policy regimes do not map cleanly to economic outcomes, but many historical episodes have shades of similarity that can help to analyze regimes and build more resilient portfolios. Policy impacts the economy, but policy regimes and economic regimes are not interchangeable. The dictates of policy often sound like clean breaks, while economic realities blur across the boundaries. Luckily, this ambiguity can be an advantage. Instead of treating policy regimes like the zero interest rate policy (ZIRP) ...

Market Signals and Shifts: What to watch in 2026

Our second annual State Street Markets outlook, Market signals and shifts: What to watch in 2026, examines the dominant forces shaping the year ahead through a lens that challenges consensus thinking.

Cross-Market Signals for the Summer

As markets enter vacation mode, this week's podcast presents our annual summer overview of the proprietary indicators available from State Street Markets and how they map to the most relevant themes driving assets and currencies. The sustainability of the tech trade in equities, the near-term path of inflation and the direction of travel for the Federal Reserve and how they feed into a rate, curve and FX view - it's all here. Host Tim Graf, Head of Macro Strategy for EMEA, talks through how unique ...

Policy Regimes versus Economic Regimes

Policy regimes do not map cleanly to economic outcomes, but many historical episodes have shades of similarity that can help to analyze regimes and build more resilient portfolios. Policy impacts the economy, but policy regimes and economic regimes are not interchangeable. The dictates of policy often sound like clean breaks, while economic realities blur across the boundaries. Luckily, this ambiguity can be an advantage. Instead of treating policy regimes like the zero interest rate policy (ZIRP) ...

What We Offer

Anticipate market trends with distinctive, data-driven measures of aggregate flow and positioning, daily inflation, media sentiment, risk regimes, and more.

Unlock new investment angles with award-winning research from collaborations with our roster of 10+ academic partners on themes including Al, private markets, investment strategies, geopolitics, and beyond.1

Gain deeper vision on market turning points, risks, and opportunities with daily views and analysis on equity, fixed income, and currency markets.

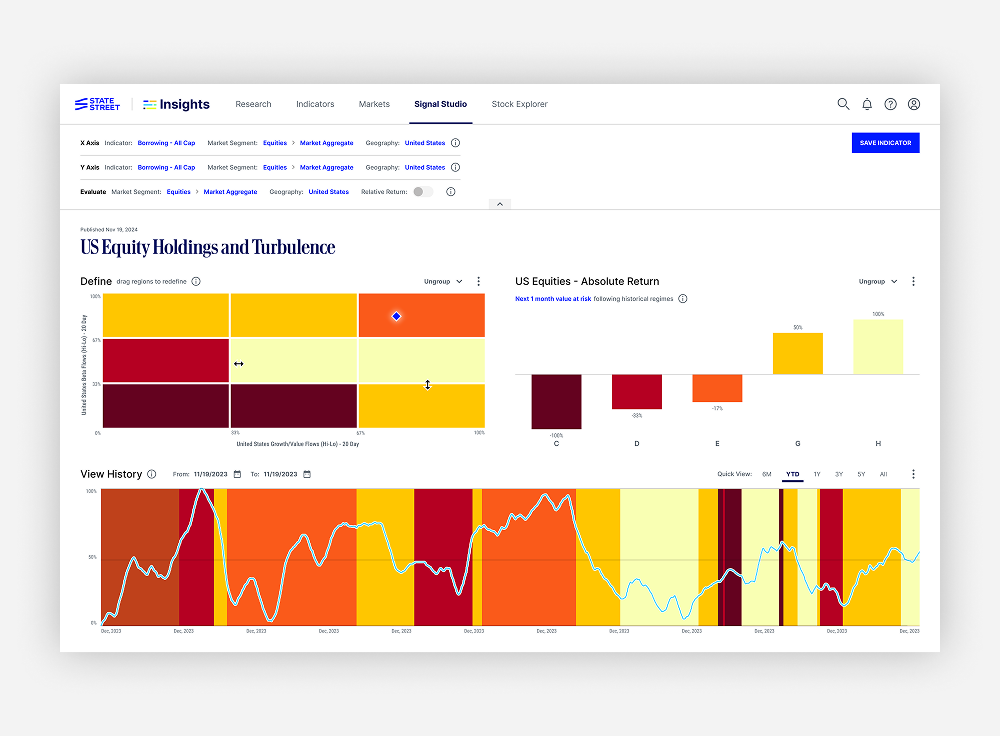

Engage with the latest analysis, interactive charts, analytic tools, calculation APIs, and more with real-time tools on our Insights platform.

Partnerships

Academic Partners

Through our network of partnerships with renowned academics, we are constantly searching for the perfect blend of deep expertise and disruptive thinking that leads to valuable ideas.

Data Partners

Strategic partnerships extend our research vision with distinctive indicators of economic and market activity, providing a real-time pulse on emerging trends and uncovering patterns that others miss.

Connect

Discussions

Interactive dialog can take ideas to new levels. Let us know how we can work together to address current challenges, extend practical applications of research, and help create new value for your team.

Events

From our flagship Research Retreat seminars to topical webinars and educational series, we bring together impactful views from research experts, policymakers, investors, and beyond.

Learn more about what Insights can do for you

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.