Factor Zoo (.zip)

By Alexander Swade, Matthias X. Hanauer, Harald Lohre, and David Blitz

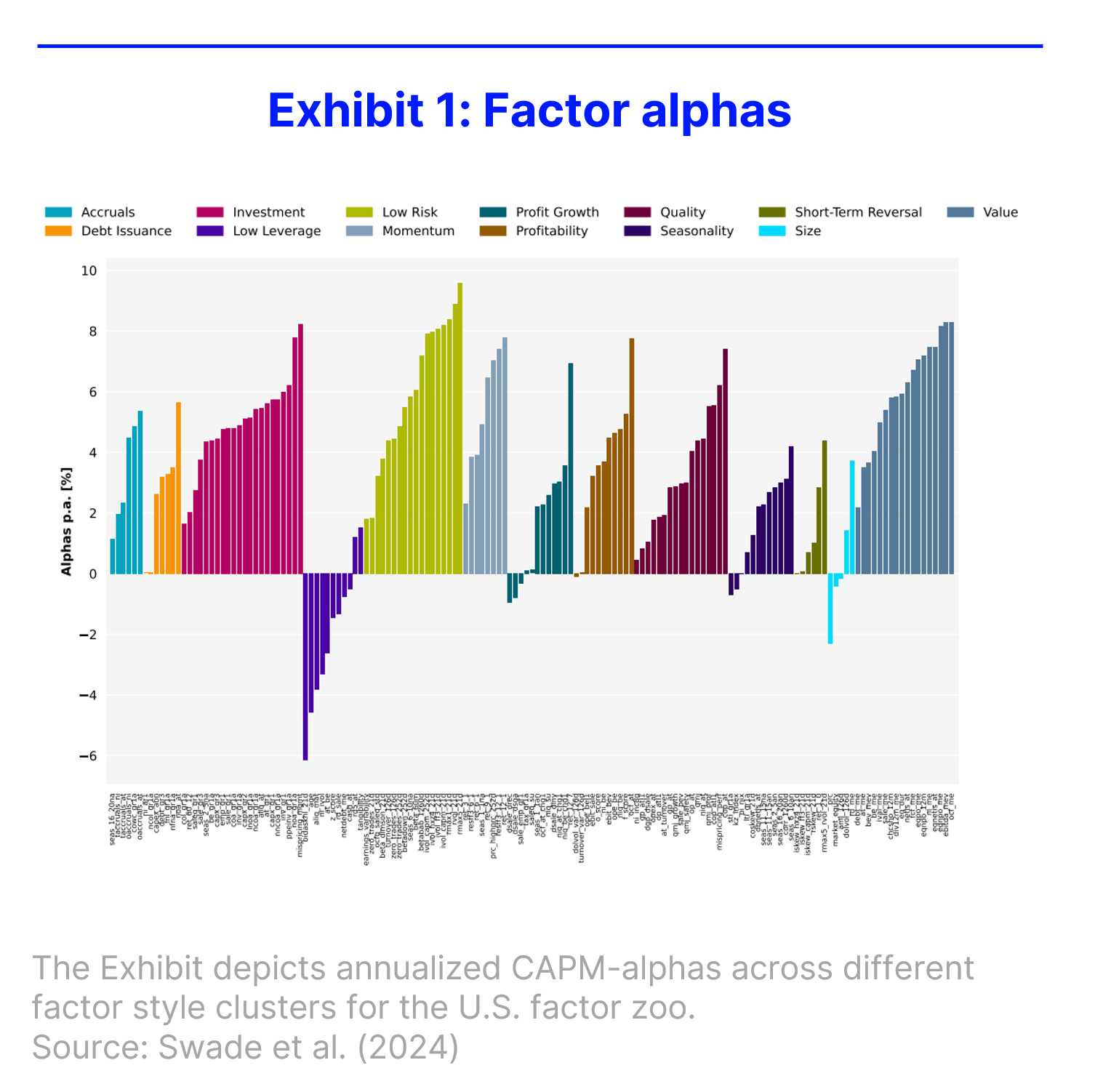

The authors propose a straightforward yet effective method to identify the factors that capture most of the available "alpha".

Since the introduction of the Capital Asset Pricing Model (CAPM), researchers have been on a quest to find the most important factors, leading to a crowded "factor zoo." Despite the variety of these factors, academic models suggested for years that most of them can be boiled down to just four to six key ones. Recent publications in this area have overcome one key challenge in sorting through this factor zoo: Not only did they reconstruct a majority of factors from the literature and publish them in open-source databases but also addressed the so-called replication crisis in finance with this approach. The authors propose a straightforward yet effective method to identify the factors that capture most of the available "alpha". These findings help investors navigate the complex factor zoo by pinpointing strong alpha contributors and comprehensive models. It also highlights the ongoing need for innovation and adjustments in models.