January 13, 2026

What to Watch

Complimentary CONTENT

Market Signals and Shifts: What to watch in 2026

By: Michael Metcalfe, Marija Veitmane, Lee Ferridge, Michael Guidi, Megan Czasonis, Ben Luk

January 13, 2026

By: Michael Metcalfe, Marija Veitmane, Lee Ferridge, Michael Guidi, Megan Czasonis, Ben Luk

Topics:

Market signals and shifts: What to watch in 2026

Our second annual

State Street Markets outlook, Market signals and shifts: What to watch in 2026,

examines the dominant forces shaping the year ahead through a lens that

challenges consensus thinking.

The outlook draws

on the work of our award-winning research team and focuses on understanding

investor behavior, regional risk dynamics and how signals evolve when markets

move away from historic norms. By combining State Street’s suite of proprietary

indicators — including a novel prediction methodology — and applying new artificial

intelligence (AI) tools to our data, we’re bringing greater clarity to a fast-shifting

market landscape that has become difficult to interpret with traditional

frameworks alone. This approach is further explained by David Turkington, head

of State Street Associates, in the accompanying video below.

At its core, Market

signals and shifts: What to watch in 2026 is designed to address the most

consequential questions investors are grappling with this year. Rather than a

point forecast, these insights can reveal market shifts and momentum changes

ahead of the broader narrative.

Read our experts’

commentary to learn:

·

Why

institutional investor asset allocation precedents are troubling

·

Whether

US equities can continue their long run of outperformance

·

What

AI and alternative data can tell us about interest rate markets

·

Whether

the US dollar can bounce back from its worst decline in almost a decade

·

Why

emerging markets should be reconsidered

As the investment

landscape grows more complex, our experienced research team remains focused on

helping investors make sense of the signals and shifts across global markets

with an eye toward identifying new opportunities and preparing for volatility.

We hope you find

this outlook useful, and we look forward to providing you with periodic updates

in the year ahead.

Tony Bisegna

Head of State

Street Markets

Troubling asset allocation precedents

Megan Czasonis, head of Portfolio

Management Research at State Street Associates and Michael Metcalfe, head of

Macro Strategy at State Street Markets

In our 2025

edition of “What to watch," we highlighted institutional investors’

overall portfolio allocation as a key issue for markets. This may be even more

important in 2026 as investors continue to allocate a historically high

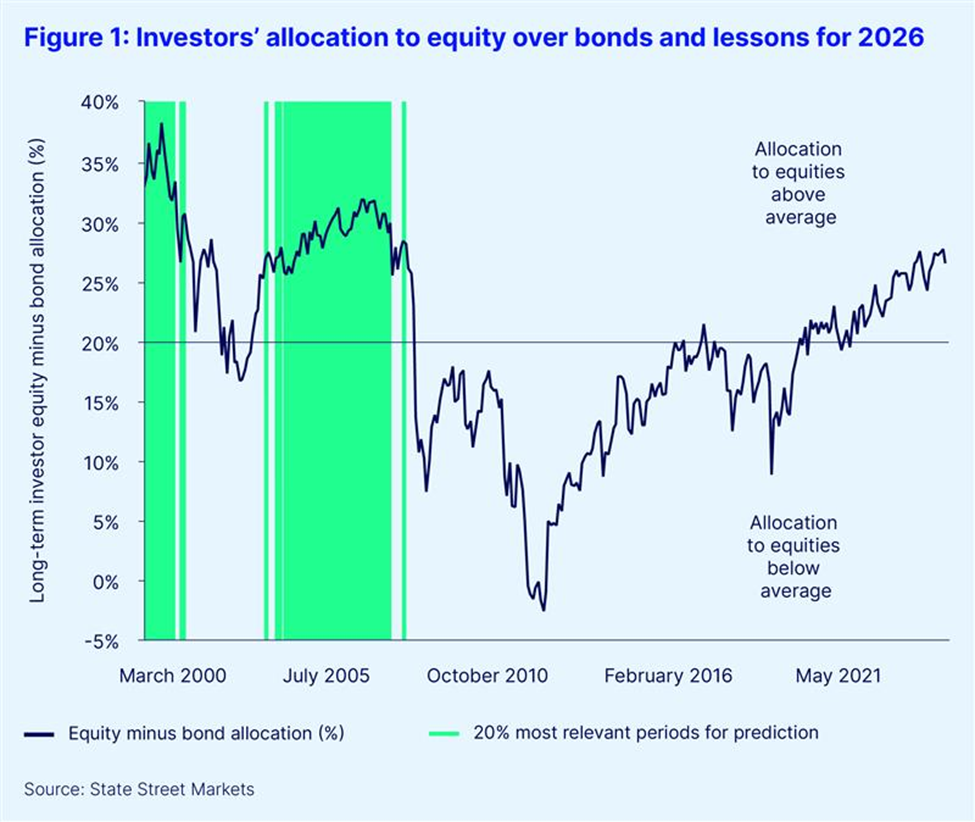

percentage of their overall portfolios to equities, relative to bonds.

According to our indicators of institutional

investor behavior, over the past 25 years the average allocation to equities

has been about 20 percent above the allocation to fixed income. This is in line

with the traditional portfolio theory of 60/40 equity/bond allocation. But as

we begin 2026, that 20 percent over-allocation to equities is above 28 percent

— a 15-year high reached this past October.

Such unusually inflated levels of optimism about

equities, especially in the face of unprecedented macro policy uncertainty and

a fundamental reorganization of the global economy, have been largely

vindicated over the past 12 months. One might assume that having passed the

stress tests of 2025, confidence for 2026 should be even higher. Nevertheless,

episodes of equity market volatility since peak optimism in October are a

reminder that with such elevated levels of equity holdings comes added market vulnerability.

What do high equity allocations mean for returns

in 2026?

Using our novel Relevance-Based Prediction

(RBP) technology,[1]

we can explore what typically happens to relative equity-bond returns following

time periods with high equity-to-bond portfolio allocations. By analyzing and

extrapolating from the most relevant past experiences, RBP generates a future

projection. In the process, it can capture complex relationships in a

transparent way.

Two things are immediately striking about the

top 20 percent of periods that were selected as most relevant to investors’

current equity overweight (see Figure 1). First, there is no recent precedent (in

the past decade). Second, the existing precedents are clustered between July

1999 and May 2001, at the peak of the dot-com bubble, and then again between

August 2004 and June 2008, during the housing bubble and the Great Financial

Crisis.

[1] Relevance-Based Prediction is a new

approach to forming data-driven predictions. For more information on the

methodology, please refer to the following papers from State Street Associates:

Megan Czasonis, Mark Kritzman and David Turkington. 2025. “A

Transparent Alternative to

Neural

Networks with an Application to Predicting Volatility.” Journal of Investment

Management,

23 (3); Megan Czasonis, Mark Kritzman, Fangzhong Liu and David Turkington.

2025. “Confidence Revisited: The

Distribution of Information.” Working Paper.

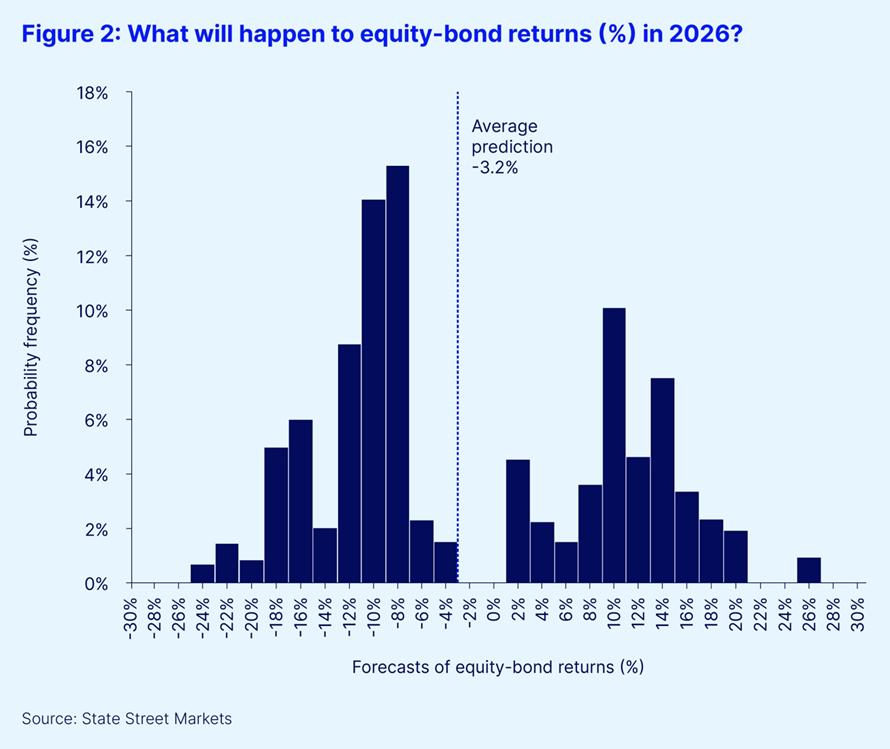

An important take-away from these relevant

periods is that they include both the build-up to the crises, when equity

returns were strong, and the eventual market crashes themselves. This is

reflected in the range of equity-bond return predictions generated by RBP from each

month in these relevant time periods. These individual or ‘solo’ predictions

represent each month’s ‘vote’ for how equities will perform next year. An

average of all these forecasts suggests that equities may underperform

bonds by 3.2 percent in the coming 12 months (see Figure 2). Interestingly, the

solo predictions are split between very negative and very positive votes,

indicating a high degree of uncertainty.

Don’t expect business as usual in 2026

At first glance, this looks like a rather

unusual way to begin a year-ahead outlook. The bimodal outcome looks to be the

statistical equivalent of the famed “two-handed economist.” And we note that it

is very different from consensus expectations, which largely forecast an average

year for equity and fixed-income returns.

But it is in keeping with typical market

outcomes during a calendar year, when mean returns are rarely observed and

outliers regularly feature. In a recent

episode of the Street Signals podcast, David

Dredge, CIO of hedge fund Convex Strategies noted, “The annual returns of the Standard

& Poor’s 500, going back to 1929 are 7.9 percent. And the frequency of that

average is three times…in 96 years. Three times. The standard deviation is 18.8

percent. What’s driving the returns? The mean or the variance? Obviously, the

variance, massively.”

This view reinforces the main takeaway from our

analysis: When allocations to equities are so high, what follows is never

average. The implications are profound. In 2026, investors need to prepare for

a range of outcomes and be ready to hedge accordingly, whether it be through

country, sector, asset, foreign exchange (FX) tilts or by employing multi-asset

and alternative strategies to

boost portfolio resilience. We’ll explore some of

these options in the following articles covering the outlook for equities,

fixed income, currencies and emerging markets.

Is US equity dominance coming to an end?

Marija Veitmane, head of Equity Research

at State Street Markets

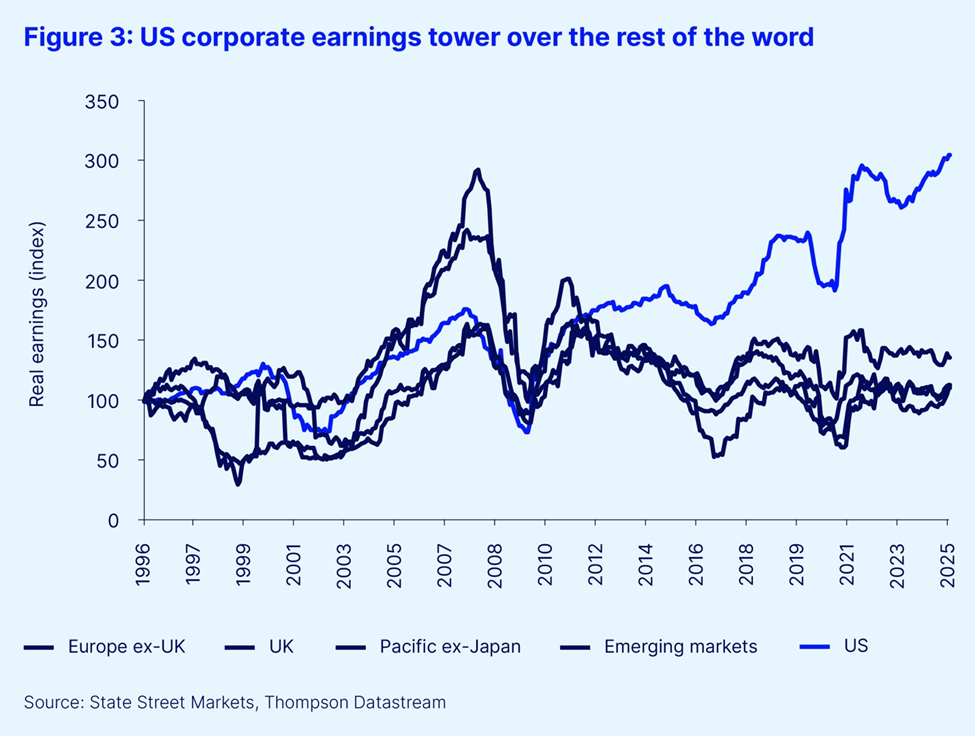

For years, United States stocks have been

favored by global investors. This preference was based on a simple idea: In a

world of sluggish economic and earnings growth, markets reward stocks with the

best earnings, and the US has had the most profitable companies (see Figure 3).

Hence, it is no surprise that US stocks have led equity markets for over a

decade now. However, this outperformance has pushed valuation and positioning

risks to high levels, indicating that earnings dominance is critical for US

stocks to continue to outperform in 2026.

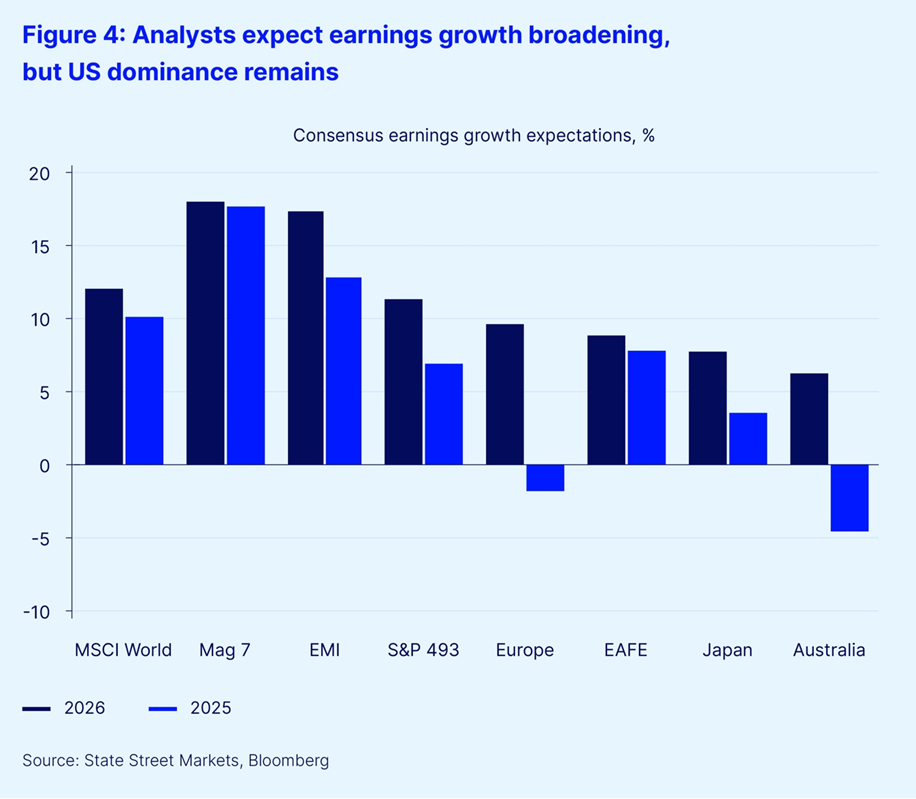

Consensus forecasts support continued US

earnings dominance in 2026

Current analyst consensus expectations support

the case for US stocks to continue to lead the rest of the world. Analysts

expect US stocks to grow earnings by 13.5 percent in 2026, ahead of just 8.7

percent for Europe, Australasia and the Far East (EAFE). Recent earnings

revisions in the US are also dominated by upgrades while the outlook for rest

of the world is getting weaker.

However, caution is still required as the majority

of earnings growth in the US is expected to come from a small group of large

stocks — the “US Magnificent 7” (see Figure 4). Indeed, earnings growth in the

US looks a lot less spectacular when we strip out these top seven technology companies,

particularly against emerging markets (EM) (see our analysis of EM later in

this outlook). Despite that, earnings expectations for US equities still

outshine most regional rivals.

Another important insight for 2026 earnings is

that analysts are yet again expecting earnings growth to broaden in other

sectors in the US and other regions in the world, potentially catching up to

the US Magnificent 7. These broadening earnings expectations have been a

consistent theme in analyst forecasts since the 2022 post-COVID-19 recovery,

yet they have failed to materialize.

Of course, past performance does not guarantee

future returns and there is no reason for past earnings disappointments to

carry into 2026, so we would recommend watching the trend in relative earnings

growth closely. Historically, the best predictors of future earnings have been capital

expenditure and operating leverage. For now, both of those drivers remain

heavily skewed toward the US, and especially technology companies.

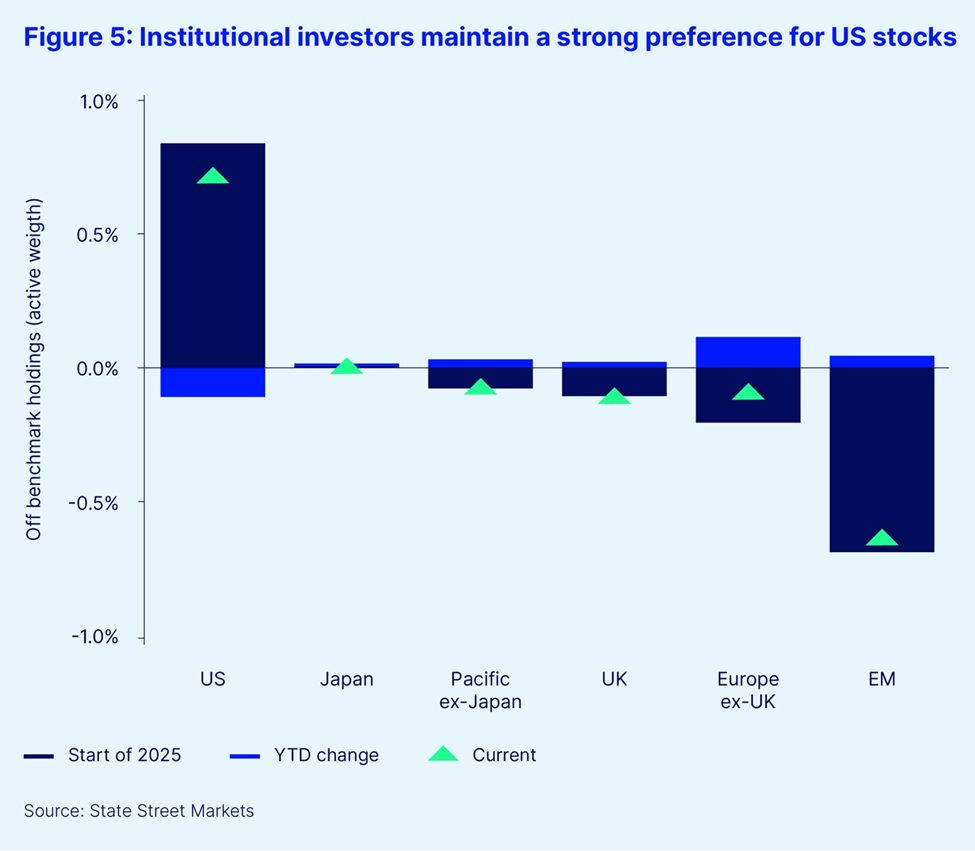

Institutional investors remain overweight in

US equities despite brief interactions with other regions

According to our Institutional Investor

Indicators, investors are maintaining a healthy degree of skepticism about

potential earnings growth outside the US. Our analysis of investor behavior

trends in 2025, alongside developments in earnings expectations, may shed more

light on investment plans in 2026 (see Figure 5).

At the start of the year, institutional

investors questioned US exceptionalism as tariffs were seen as a supply shock

(potentially raising prices and slowing economic growth) making it hard for the

Federal Reserve to reignite the economy if needed. As a result, they shifted to

some degree from the US to Europe, where the potential for a fiscal boost

supported earnings growth expectations. However, a European earnings recovery has

failed to materialize (currently EPS growth is expected to end the year at -2 percent)

and institutional investors abandoned European stocks.

Later in the year, investors were encouraged by

the Chinese authorities’ efforts to boost domestic demand and they reduced

their underweight positions there. Yet once again, earnings growth failed to

materialize (currently also tracking at -2 percent year-on-year) and

institutional investors increasingly lost interest. Instead, we now see investor

appetite for Latin America and tech-heavy Asian stock markets increasing, where

earnings expectations remain solid.

Finally, recent elections in Japan have

rekindled investor interest there with the hopes that a more expansionary

Japanese fiscal policy and new structural reforms could boost earnings growth.

Yet here too, worries that inflation may strengthen the Japanese yen seem to be

dampening recent enthusiasm.

After having ventured into different markets

this year, institutional investors have shown a preference for continuing to

invest in what they perceive as reliable earnings growth in the US. In fact, we

have seen nearly six months of uninterrupted buying of US equities from

institutional investors.

In conclusion, we believe that the key factor

to watch for with regard to regional equity allocation is relative earnings

growth. For years, the profitability of US companies has towered over the rest

of the world, which was rewarded by multi-year outperformance. Analysts, as is

customary for their year-ahead analysis, are looking for earnings growth to

broaden regionally. Yet institutional investors, and we here at State Street

Markets, are yet to be convinced.

What AI and alternative data reveal about interest rate markets in 2026

Michael Guidi, head of Alternative Data at

State Street Associates and Michael Metcalfe, head of Macro Strategy at State

Street Markets

In 2025, financial

markets were shaped not just by the anticipation of AI-driven returns, but also

by shifting expectations around central bank interest rate policy. These

expectations led to significant moves in both short- and long-term interest

rates, with ripple effects across asset classes. As we enter 2026, a key question

is, “What can AI and alternative data — especially tools like State Street

PriceStats — reveal about the likely divergence in interest rate markets?” And

even more critically, how might these insights help us anticipate the next move

in short- and long-term rates?

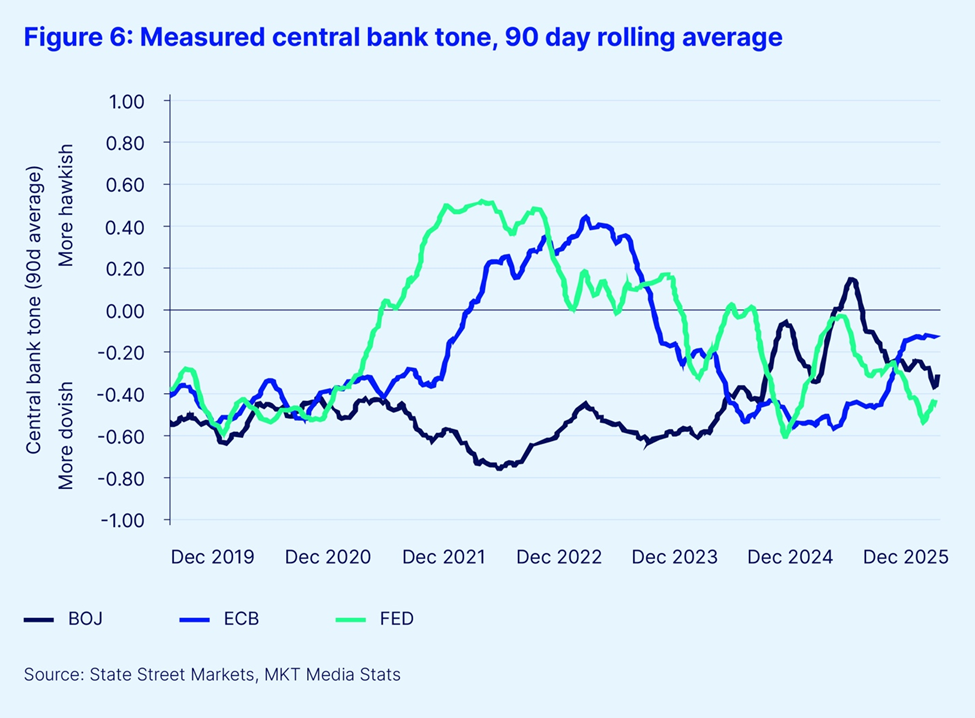

The power of language analytics

to determine central bank tone

Central banks are

prolific communicators, aiming to guide market expectations and smooth the

impact of their policy decisions. The financial media amplifies these messages,

often highlighting the most market-relevant statements. Large language models

(LLMs) now enable us to systematically analyze this vast communication flow. In

partnership with Fintech company MKT MediaStats, we can classify central bank

statements and media coverage as “hawkish” (favoring tighter policy) or

“dovish” (favoring easier policy), and construct real-time indicators of

monetary policy sentiment. In our experience, we have found that these

AI-driven tone measures are valuable tools for forecasting policy shifts.

At the start of 2025,

the European Central Bank (ECB) was the most dovish among the major central

banks, but after its final rate cut in June, its tone shifted and it is now the

least dovish of the G3 (see Figure 6). Meanwhile, the Bank of Japan (BoJ) and

the Federal Reserve have shown more variation in their tone. The BoJ, after

years of ultra-accommodative policy, is now only slightly more dovish than the

ECB, reflecting tentative normalization and a desire to avoid further yen

weakness.

The Fed, by contrast,

became markedly more dovish from June onwards and has since delivered rate cuts

at the last three meetings of 2025. But we would be cautious about

extrapolating from that. Our AI-based tone analysis also quantifies the degree

of disagreement among individual central bankers, revealing the highest levels

of internal divergence in over four years at the Fed. This suggests a

heightened risk of policy surprises and market volatility, and implies the Fed

will continue to stress a “data-dependent” approach.

Real-time insights from

alternative inflation data

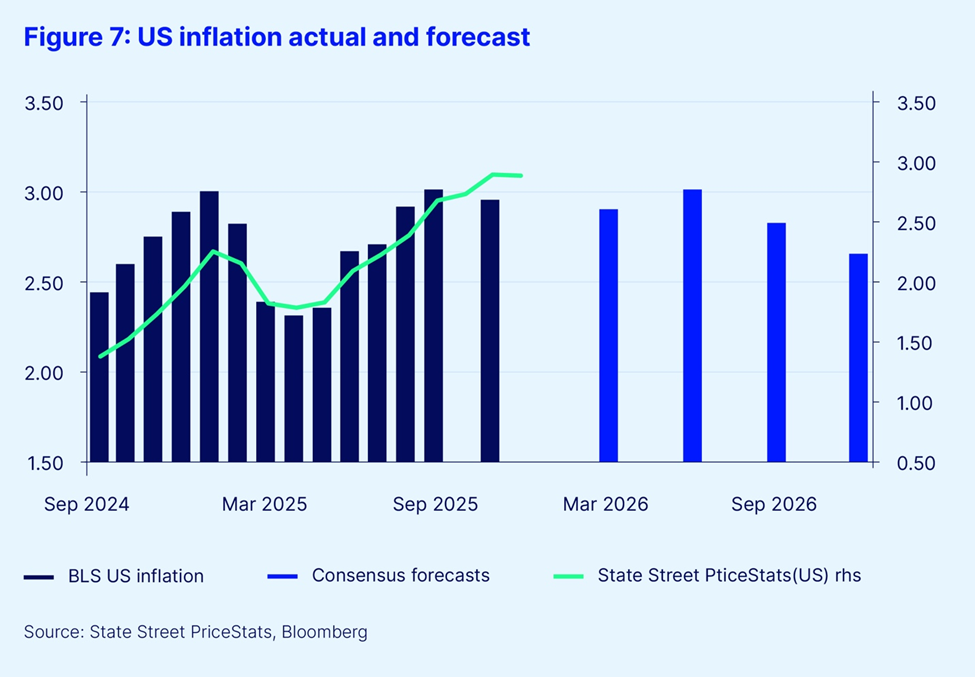

The debate within the

Fed’s chief policy-making body, the Federal Open Market Committee (FOMC), will

ultimately be shaped by the path of inflation. Despite volatility, US inflation

ended 2025 close to mid-year forecasts. State Street PriceStats, a

high-frequency inflation tracker, has proven especially useful — capturing

downside surprises in official data in early 2025 and the summer’s inflation

reacceleration, and even substituting for official data during the fourth

quarter US government shutdown.

As 2026 begins, State

Street PriceStats shows US annual inflation, particularly in goods, plateauing

and starting to roll over in line with forecasts (see Figure 7). If the labor

market continues to soften, this should reduce Fed disagreements and pave the

way for further Fed easing, moving rates back toward neutral as the consensus

expects.

What is perhaps an even

more revealing finding from State Street PriceStats is the recent

re-acceleration of inflation in Europe, and deceleration in Japan (albeit from

an elevated level). This divergence mirrors the shifts in central bank tone and

points to a more fragmented global economic outlook. For Europe, it suggests

the next rate move could be upward, in line with the ECB’s more balanced tone.

For Japan, again following the tone, it signals that any tightening cycle will

likely be cautious and shallow.

A divergence in demand

will drive bond markets in 2026

The BoJ’s caution is

rooted in nearly two decades of disinflation and a desire to avoid disruptions

in long-term yields. Across asset classes, the message is again one of

divergence. Throughout 2025, asset manager demand for 30-year US Treasuries was

below average for all but one month. Conversely, demand for Eurozone and

Japanese sovereign debt from international investors was above average.

In the second half of

2025, more constructive price action in the US Treasury market suggests that

other investor segments have stepped in to fill the gap. However, few sources

of demand are as stable as long-term asset managers. If these buyers do not return

in 2026 and the Fed continues to cut short-term rates, the risk of greater

volatility in yield and yield curve steepness looks to be higher in the US than

elsewhere.

Overall in 2026, we expect an unusual

divergence in G3 policy rates and continued risks at the long-end of the US

curve.

Dollar bounce or more of the same?

Lee Ferridge, head of Multi-Asset Strategy

for the Americas at State Street Markets

2025 was a tough year for the US dollar. The US

Dollar Index (DXY) has fallen by 9.4 percent so far this year; its worst annual

performance since 2016 and the second worst since 2003. You might expect that what

goes down must come up — but is that always true?

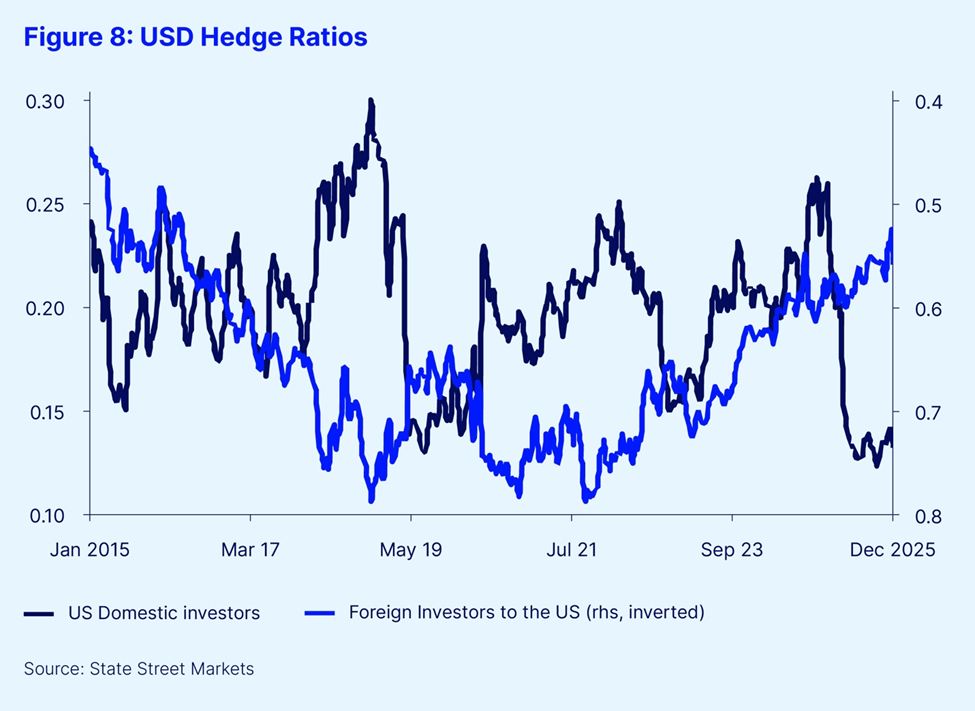

One of the most notable takeaways from our US

Dollar Investor Behavior Indicators is that, despite the USD’s poor performance

in 2025, overseas owners of US financial assets did not materially increase

their USD hedge ratios this year (see Figure 8). That means they maintained

their exposure to the USD in the face of its decline.

As Figure 8 illustrates, rather than overseas

investors increasing their USD hedge ratios in 2025, they have actually reduced

them slightly, from close to 58 percent at the start of the year, to 56 percent

now. At its nadir in 2025, the overseas USD hedge ratio fell to just under 53

percent; its lowest level since 2016.

When it comes to FX hedging activity, it was US

domestic investors who had the most pronounced reaction in the lead-up to, and

immediately following, the “Liberation Day” market volatility. US investors

more than halved the hedge ratio on their foreign currency exposures (i.e.,

they sold USD) from around 25 percent at the start of 2025, to a low of a

little above 12 percent. The current reading is just over 13 percent. In large

part, US investors were behind the dramatic sell-off in the USD seen in the

first half of this year.

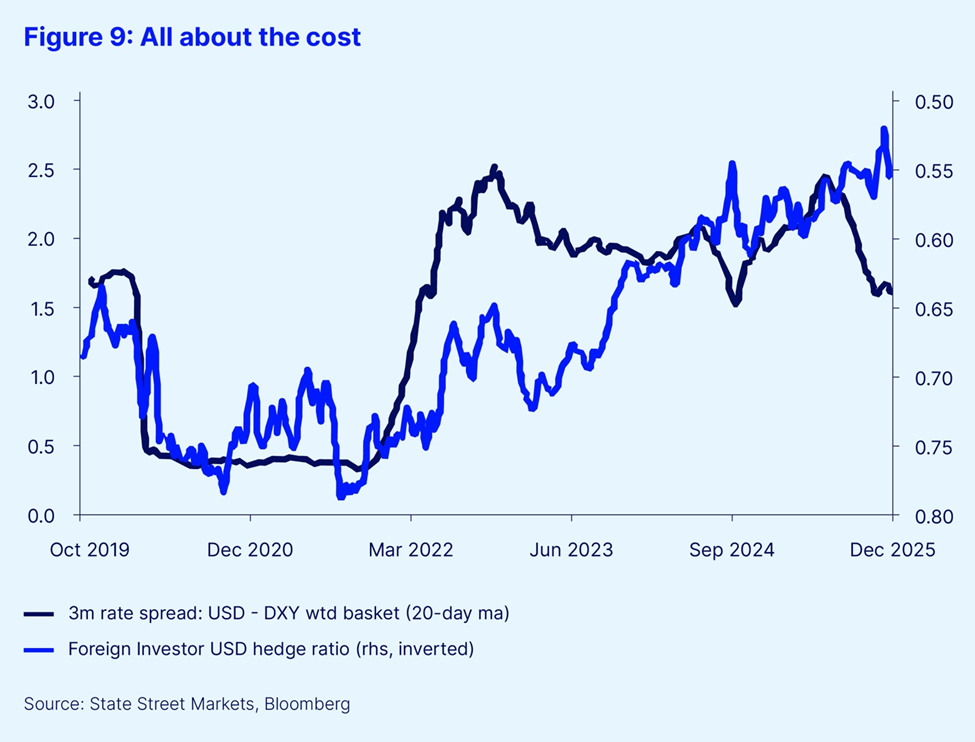

The next question to consider then is, “Given

the USD’s poor performance, why did foreign investors hold firm?” Why didn’t

they increase their USD hedge ratios, thereby reducing their exposure to a declining

USD?

The answer is captured in Figure 9. As our

chart illustrates, the decision over how much to hedge USD exposure is heavily

influenced by the cost of the hedge. In early 2022, before the FOMC started its

post-COVID-19 hiking cycle, it was effectively free for overseas investors to

hedge their USD risk. At that time, our USD Foreign Hedge Ratio Indicator was

at 78 percent. Since then, it has steadily declined due to rising hedging costs

for overseas investors converting to USD. Although the US interest rate premium

over a DXY-weighted G10 index has narrowed in recent weeks, foreign investors

will still, on average, be giving up around 1.5 percent of their returns to

hedge the USD.

However, when we look ahead to 2026, consensus

expectations suggest that this hedging cost will fall meaningfully over the

coming quarters. The FOMC is currently priced to cut a further two times in

2026. While not particularly significant, it stands in sharp contrast to the

interest rate expectations across much of the G10, as highlighted earlier in

this 2026 outlook (see Figure 3).

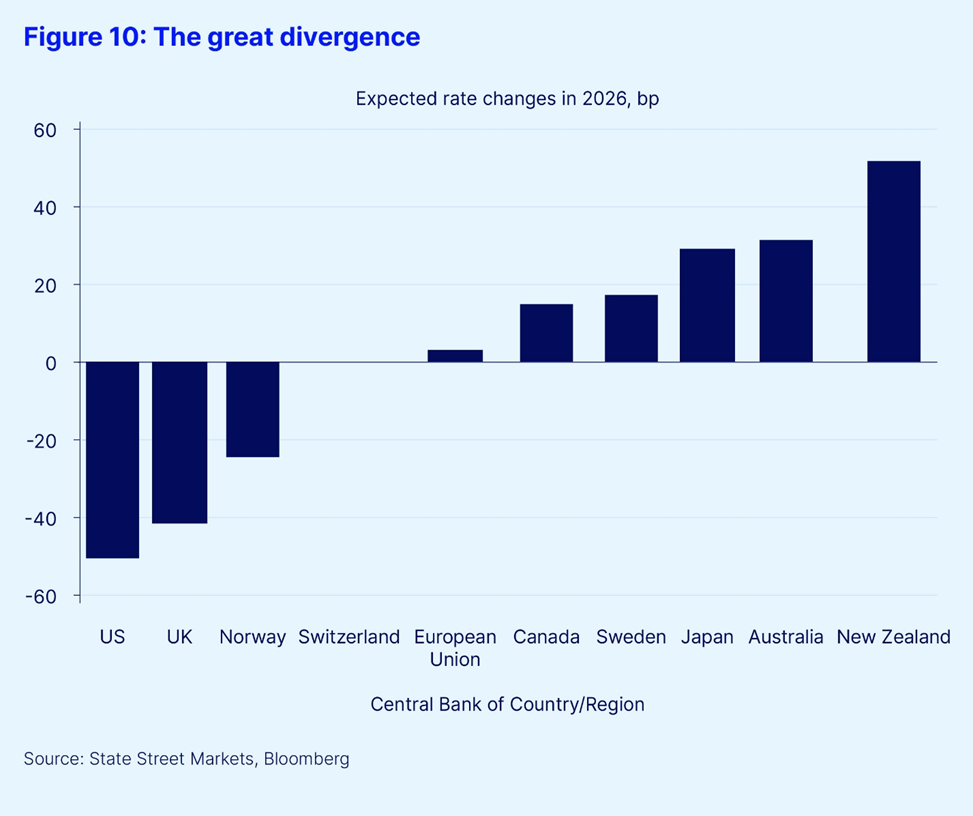

As Figure 10 illustrates, the FOMC is expected

to ease by more than any other G10 central bank in 2026. Additionally, five of

the G10 central banks are currently expected to raise rates next year. If these

consensus expectations are realized, 2026 would represent a very unusual year

of divergence in G10 central bank policy. The last time three or more G10

central banks diverged in policy was in 2004.

Indeed, since 2019, only the BoJ has moved counter to the majority. Perhaps

even more significantly, the Fed is poised to cut rates next year (along with

the Bank of England and Norges Bank).

Whether others will hike while the

Fed is easing remains to be seen. However, if market pricing proves accurate,

2026 could be an interesting FX year for the USD. In 2004, when the Fed was

cutting rates while more than three other G10 central banks were raising rates,

the DXY fell by 7 percent, having fallen by 15 percent the previous year.

In answer to the question posed at

the start, what goes down does not necessarily have to go up the

following year. With overseas USD hedge ratios at historically low levels and

the cost of hedging USD exposure set to fall in 2026, a USD bounce in 2026

seems unlikely.

Rerating emerging markets: From cyclical to structural ownership

Ben Luk, senior multi-asset strategist at

State Street Markets

EM

had a stellar year in 2025, with double-digit gains across carry, bonds and

equities. This rally was due to a combination of external and internal

tailwinds, which led to better inflows across the region. A weak USD backdrop,

coupled with a significant decrease in cross-asset volatility, encouraged

investors in EM, while macro conditions surprised on the upside, thanks to

strong demand for AI-related products despite persistent tariff threats. Last,

but not least, credible central bank policy and prudent government spending underpinned

confidence in EMs.

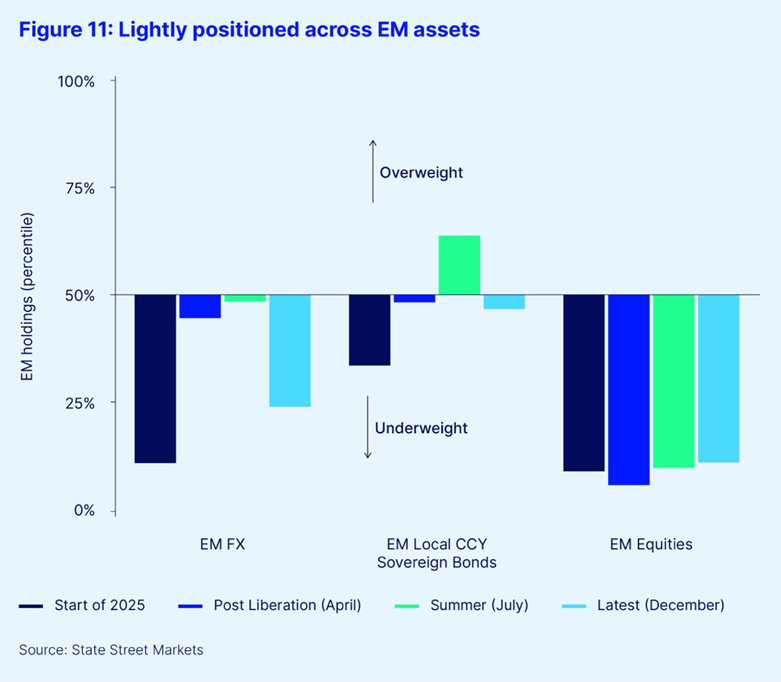

Yet

surprisingly, as we begin 2026, according to our Institutional Investor

Indicators (see Figure 11), institutional investors have remained on the

sidelines with underweight positions across EM FX, local currency sovereign

bonds and equities. This makes the region an attractive opportunity for

investors seeking to diversify away from overweight positions in both Europe

and the US.

Unlike their developed market (DM)

counterparts, EM central banks were not aggressive in easing policies over the

past 12 months as they managed to build hefty FX reserves during a weak USD

environment to potentially offset capital outflows. According to State Street

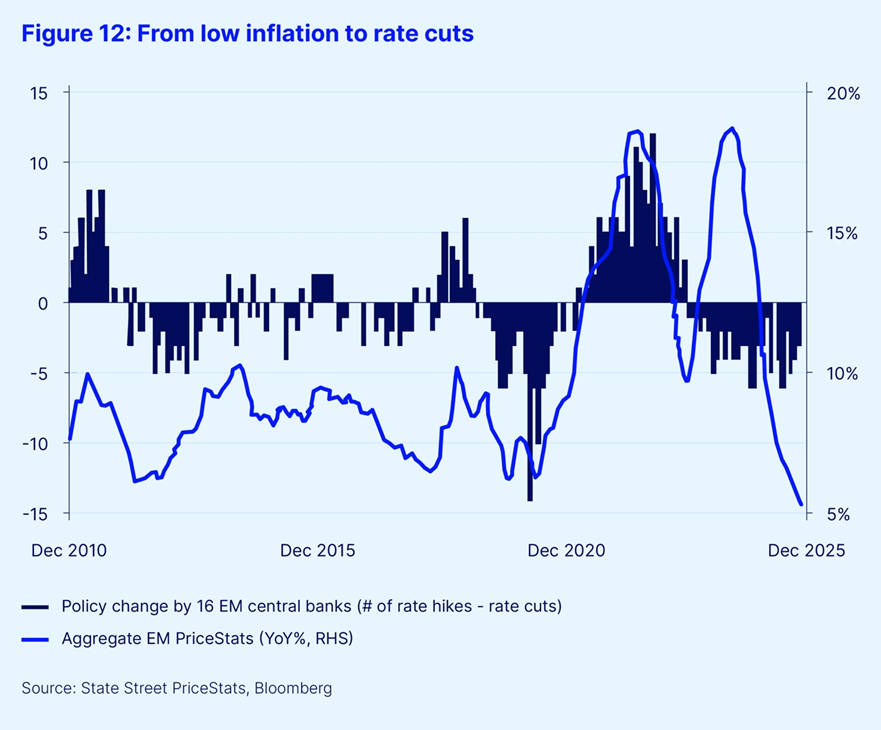

PriceStats, aggregate EM online prices have fallen 5.2 percent year-on-year;

the lowest reading in the past 15 years, whereas DM inflation is back to a three-year

high (see Figure 12). This divergence in price dynamics has forced DM central

banks to keep rates anchored, whereas EM central banks can still cut rates in

the medium term due to lower underlying inflation dynamics — although markets

have priced in a lot of easing going into 2026. Moreover, US Treasury movements

this year have been driven not only by cyclical factors, but also by structural

concerns such as debt sustainability, central bank independence and the future

trajectory of Fed Chairman Powell; still, EM bonds have demonstrated resiliency

in 2025.

We anticipate EM yield differentials to

compress further in 2026. However, active management will be essential to

determine which countries and which parts of the curve to invest in, as

idiosyncratic factors such as elections, defaults or renewed geopolitical

tensions may arise — even if EM central banks collectively look to extend their

easing cycles. Investors should consider this asset class not as a cyclical

trade, but as a long-term strategic allocation, as foreign ownership remains

well below long-term average.

Monetary policy serves as a foundation for the

stability of Ems, but what matters in the long run is economic growth and

trade. World trade has continued to strengthen despite tariff threats, while

economic surprises in EM have turned positive since the start of the fourth

quarter. In 2026, gross domestic product (GDP) growth in EM is expected to

remain unchanged at 4.1 percent, similar to growth levels seen in 2025 and

2024.

We expect EM exports to remain resilient next

year given the ongoing surge in AI and chip innovation, as China, South Korea

and Taiwan are the major beneficiaries of the global technology cycle. However,

China’s growth will likely remain under pressure due to geopolitical tensions

with the US (and most recently, Japan), but this could force Beijing to be

proactive instead of reactive. Policymakers are focused on policies to fight

against deflation, and Beijing should encourage consumer spending, self-sustainability

and high-value-chain manufacturing, as well as provide indirect support to the

property and labor markets. We see the potential for continued positive equity

performance in 2026, as corporate earnings improve due to Asian tech proxies

while investors take advantage of the deep valuation discount relative to US

equities.

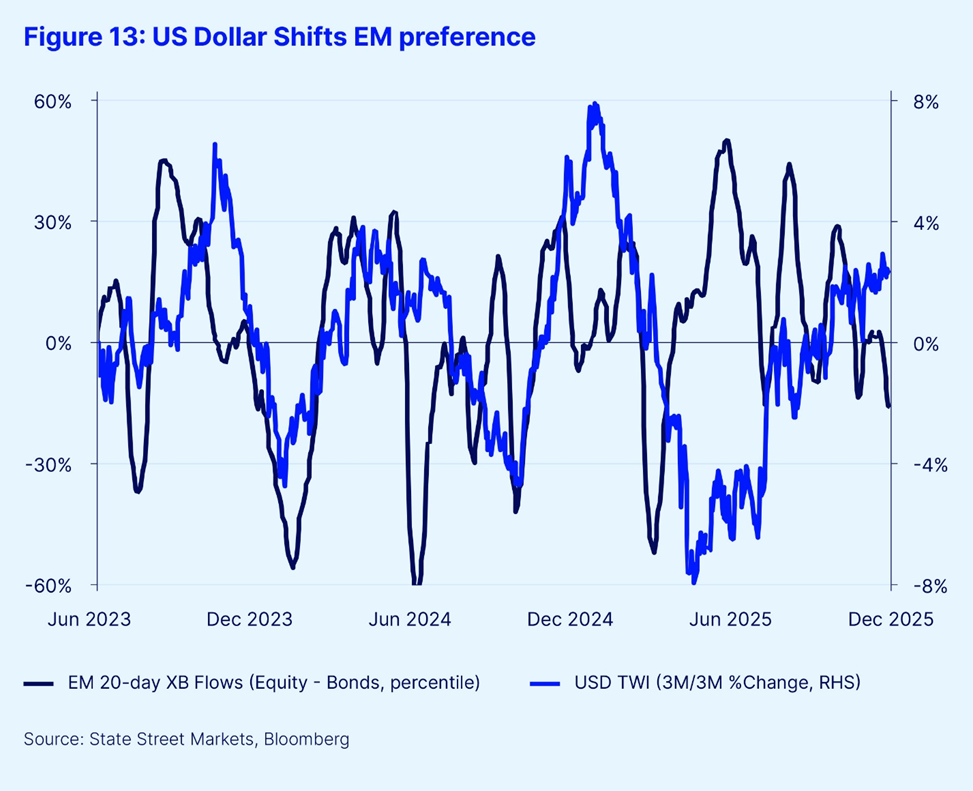

The biggest concern for EM has, and will always

be, renewed USD strength — although not all EM assets are as vulnerable. As we

track real money flows over time, we have observed a rotation in investor

preference of EM equities over bonds in a rising dollar environment, but not a

diversion from the entire region (see Figure 13). EM bond managers are more

sensitive to USD strength, as gains in FX would be wiped out and spreads would widen

while hedging costs would increase. On the contrary, weaker EM currencies can

still benefit from equities if this translates into stronger exports and

greater market share — ultimately leading to higher earnings growth.

Investors have aggressively sold EM in the past,

given a downturn in growth and a lack of accountability from central banks and

the government; but the EM of today are not the same as in the past. Credible

policy management and improving fiscal balances, coupled with steady macro

conditions, indicate that EM as a whole deserve more attention, especially for

investors looking to expand their risk spectrum and increase their

diversification. As we enter 2026, EM as an asset class remains extremely

under-owned and undervalued.

Disclaimer & Risk

Author Bios

Michael Metcalfe

Michael is Senior Managing Director and Head of Macro Strategy at State Street Markets

Marija Veitmane

Marija Veitmane is Managing Director and Head of Equity Research at State Street Markets

Lee Ferridge

Lee Ferridge is Senior Managing Director and North American Head of Macro Strategy at State Street Markets

Michael Guidi

Michael Guidi is a member of the Investor Behavior Research team at State Street Associates (SSA). Since joining SSA in 2011, Michael’s research has spanned multiple product lines including our behavioral indicators, media sentiment products, and high-frequency inflation indicators. He holds a Bachelor of Science in electrical and computer engineering from University of Florida, a MS in mathematical finance from Boston University, and the CFA charter.

Megan Czasonis

Megan Czasonis is a Managing Director and Head of Portfolio Management Research at State Street Associates. Her team collaborates with academic partners to develop new research on asset allocation, risk management, and quantitative investment strategy. The Portfolio Management Research team delivers this research to institutional investors through indicators, advisory projects, thought leadership pieces, and interactive tools. Megan has published numerous journal articles, is a co-author of “Prediction Revisited: The Importance of Observation,” and her research received the 2022 Harry Markowitz Award for best paper in the Journal of Investment Management. Megan graduated Summa Cum Laude from Bentley University with a B.S. in Economics / Finance.

Ben Luk

Ben Luk is Vice President and Senior Multi-Asset Strategist at State Street Markets

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.