November 3, 2025

Working Papers

Complimentary CONTENT

The media short squeeze score

By: Travis Whitmore, Junming Cui, Gideon Ozik, Ronnie Sadka, Michael Guidi

November 3, 2025

By: Travis Whitmore, Junming Cui, Gideon Ozik, Ronnie Sadka, Michael Guidi

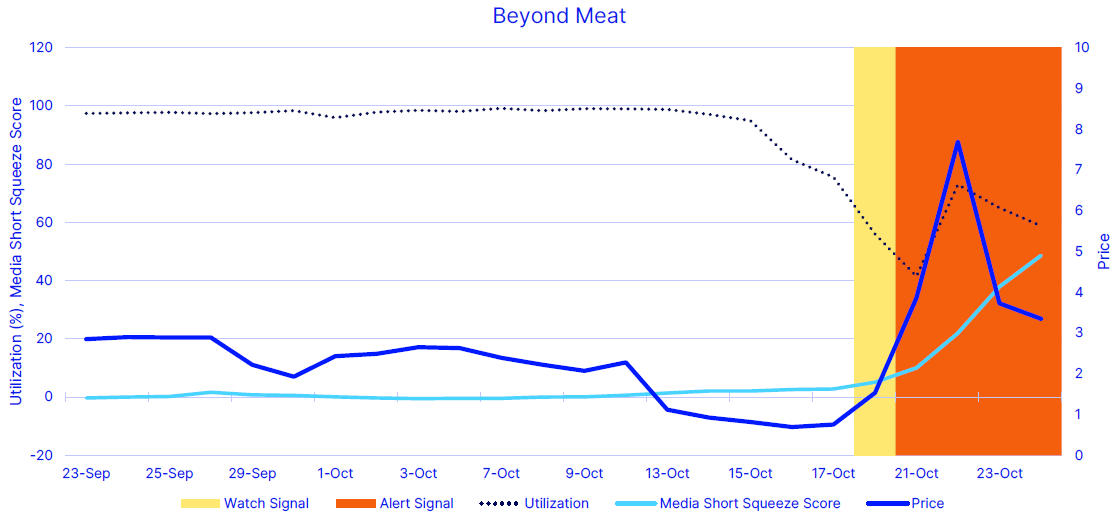

The meme stock phenomenon remains a persistent force in equity markets, with retail investors continuing to exert significant influence – particularly in the small-cap segment. While it has been several years since the first GameStop phenomenon in 2021, an important question remains: How can institutional investors systematically identify potential retail-driven short squeeze events? In this article, we introduce a framework that integrates proprietary and alternative data to identify retail-driven short squeeze risks. Specifically, we combine securities lending market data from S&P Global with proprietary measures of digital media sources and Reddit-based social media chatter – including emoji sentiment and short squeeze intensity.

Author Bios

Travis Whitmore

Travis Whitmore is a senior quantitative researcher at State Street Associates, the partnership between State Street Markets and renowned academics at Harvard Business School, MIT Sloan School of Management, Boston College and EDHEC Business School. Based out of Frankfurt, he works with institutional clients in continental Europe across State Street Associate’s entire research offering and helps drive global research initiatives. Before moving to his role in Frankfurt, Travis worked closely with Harvard Professor Ken Froot to develop new investment applications with our proprietary flows and holdings information. Additionally, he worked with the academic partners at MediaStats, a firm specializing in Natural Language Processing, to help investors leverage digital media indicators in their decision-making.

Junming Cui

Junming Cui is a quantitative researcher at State Street Associates. Junming’s research focuses on evaluating alternative data, examining its relationships with traditional and proprietary factors, and leveraging these insights in the development of quantitative investment strategies. Junming received his Bachelor of Science in Honors Mathematics from New York University and Master of Finance from MIT.

Gideon Ozik

Gideon is a managing partner and founder of MKT MediaStats, where he leads business, research, and development. He has applied quantitative research in roles spanning investment solutions, hedge funds, and derivatives trading, and he is an affiliate professor at EDHEC. His research focuses on advancing unstructured data analysis using AI and machine learning to extract actionable signals from media. Gideon’s contribution to research and product development provides State Street clients with a unique lens on the implications of media for markets.

Ronnie Sadka

Ronnie is a professor and chairperson of the finance department at the Carroll School of Management at Boston College. He is also a managing partner and founder of MKT MediaStats, which produces innovative measures of financial economic narratives from online media. In addition to his research on narratives, he has published extensively on liquidity in financial markets. Ronnie’s contributions advance the development and application of alternative data sets for State Street clients.

Michael Guidi

Michael Guidi is a member of the Investor Behavior Research team at State Street Associates (SSA). Since joining SSA in 2011, Michael’s research has spanned multiple product lines including our behavioral indicators, media sentiment products, and high-frequency inflation indicators. He holds a Bachelor of Science in electrical and computer engineering from University of Florida, a MS in mathematical finance from Boston University, and the CFA charter.

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.