The cost of clearing repo analysis

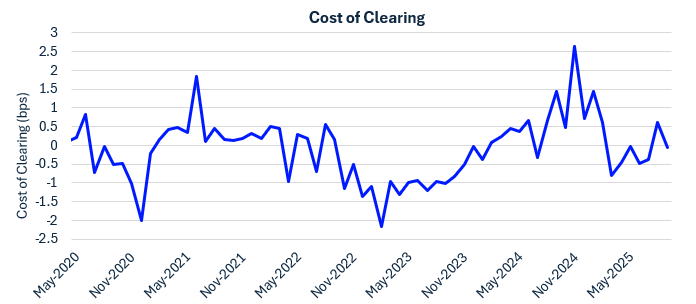

The forthcoming SEC mandate for central clearing of U.S. Treasury repo transactions by 2027 is expected to materially alter market structure, particularly for buy‑side cash lenders such as money market funds (MMFs). Using a month‑end panel of MMF holdings from 2020–2025, we estimate the cost of clearing, defined as the spread between uncleared and cleared repo rates, and examine its drivers in a regression framework. We find that higher FICC Sponsored volumes are associated with lower clearing costs, consistent with netting efficiencies and economies of scale, while larger MMF balance sheets tend to widen the spread, an effect partially offset by higher MMF repo activity. Collateral supply and broader liquidity conditions, including SOMA holdings, net UST issuance, and dealer balance‑sheet constraints, also play an important role. Overall, the results suggest that the cost of clearing is a macro‑sensitive spread rather than a fixed wedge, and that increased clearing volumes under the mandate are likely to structurally compress clearing costs, with implications for pricing, venue choice, and liquidity management for buy‑side lenders.