November 26, 2025

What to Watch

Complimentary CONTENT

Market Signals and Shifts: An end-of-year assessment

November 26, 2025

By: Michael Metcalfe

- Michael MetcalfeSenior Managing Director

By Michael Metcalfe, Head of Macro Strategy

In our January 2025 look-ahead

report, we pinpointed several critical fault lines and promising updrafts

for financial markets. Among the questions we sought to answer during the year were:

Will United States’ exceptionalism continue to dominate market consensus, or

are we on the brink of a significant shift away from the US? Where does the US

dollar go from here? Will Treasuries get some traction?

With less than two months remaining in 2025, we assess key

developments on these topics and more, and look ahead to what we expect will

matter most for markets in 2026.

Will investors remain overweight equities?

Despite a few wobbles this year, the answer to that question

has been a definitive “yes.” Investors entered 2025 with a high allocation in

equities relative to bonds. Over the past 25 years, the average allocation to

equities has been around 20 percent above the allocation to fixed income, in

line with the 60/40 portfolio. In January, it reached 7.5 percent above this

long-run average — a 15-year high. After

a violent wobble in the second quarter, it returned to and then surpassed this

high in the third quarter (See Figure 1).

This leaves asset manager allocations to equities stretched back

to levels seen only in the run-up to August 2000 and July 2007. These are, of

course, troubling precedents, but so far investor sentiment has passed all the

stress tests that 2025 has thrown at it. In particular, it is the first time

that a Federal Reserve easing cycle has coincided with a lower, not higher

allocation to bonds relative to equities.

As we highlighted back in January, this easing cycle looked

like it may be somewhat different, and that has proven to be the case 10 months

later. This leaves the large overweight in equities as a continued point of

caution for 2026. At present, however, investor appetite for equity over bond

risk remains remarkably resilient.

Can the US and US tech remain exceptional?

Not only are investors overweight equities, as mentioned above,

but within equities the US is still the only overweight across

regions.

By the end of March, investors’ holdings of US stocks above

benchmark weight had been reduced by around one-fifth, and there was a

flirtation with above-benchmark holdings in European stocks. But this proved

brief.

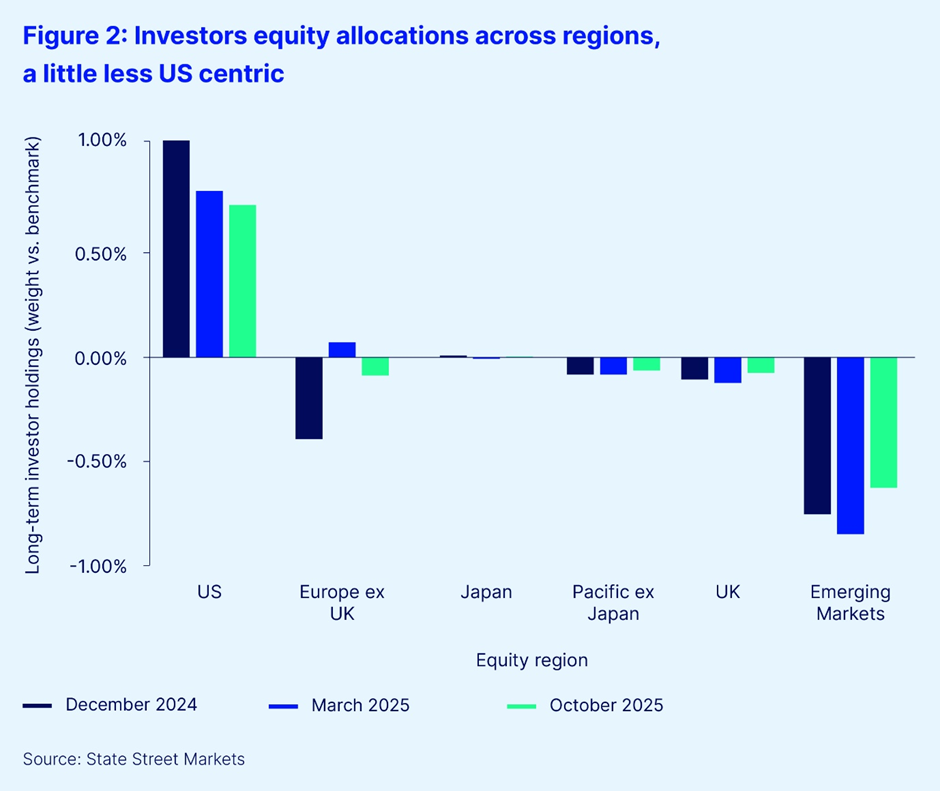

Holdings of European stocks were back to a small underweight

by October, as shown in Figure 2, while overweight holdings in US equities had

slipped slightly, and underweights in UK and emerging markets were somewhat

reduced. It may be inferred that the US, from an equity viewpoint, is a little

less exceptional than it was in December 2024, but only marginally so. That

concentration will, of course, remain a potential risk going into 2026.

But a little like the equity overweight itself, it is a risk

that was stress tested robustly in 2025 and appeared to pass. As our Global Head

of Equity Strategy, Marija Veitmane, argued back in January, it is a view

supported by robust relative earnings growth, and this has held true through

all three earnings seasons this year. In short, US equity exceptionalism was

and is a well-earned narrative. However, strong earnings growth in Japan and

emerging markets present alternative opportunities that should be closely

watched.

Is there trouble ahead for Treasuries?

As exceptional as investor demand has been for US equities,

the same has not been true for other asset classes. When we asked this question

back in January, we were concerned that a combination of fiscal issues,

potentially higher inflation and weaker asset manager demand would lead to

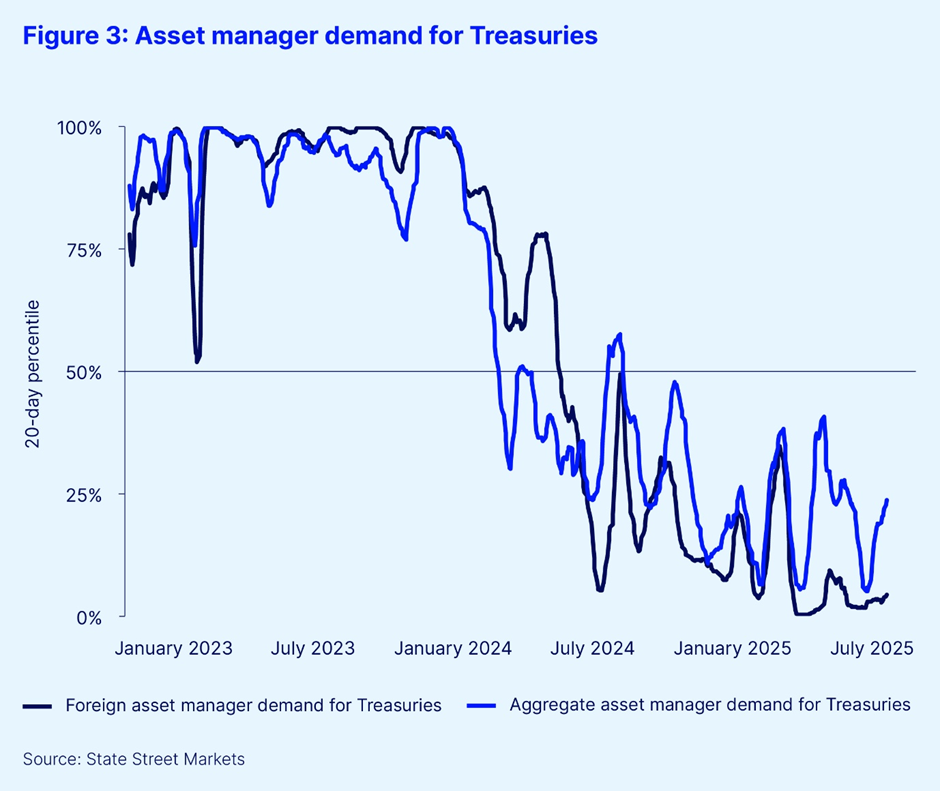

higher long-dated yields at the very least. Yet, while 2025 has not been an

easier year for fixed-income managers, 10 months later, 10- and 30-year Treasury

yields are back below where they began the year. (See Figure 3.) If there was

trouble for Treasuries in 2025, it was short-lived.

However, this doesn’t imply that concerns have gone away

completely. The US budget bill has locked in significant fiscal stimulus and

increased Treasury supply. Inflation has also reaccelerated over summer, but

more recent data from State Street PriceStats shows that inflation may be

fading as the year ends. After lurching higher at the beginning of the year,

inflation forecasts have been largely stable and are still projected to decline

in 2026.

Against that background, though, it is notable (and our data

reveals) that asset manager demand for Treasuries has remained below average,

especially from non-US managers and particularly at longer-dated durations. The

lesson from 2025 is that stronger Treasury demand from other sources like retail

investors, commercial banks and leveraged investors has been sufficient to

offset this weakness. So it appears this will remain a potential risk for 2026

to the extent that asset manager demand is typically one of the more stable

sources of demand for sovereign bonds. But with market hopes that the US Federal

Reserve may resume its Treasury purchases in 2026 and issuance focused on the

front end of the curve, these risks may be more modest next year.

Will US dollar strength persist?

“Definitely not,” was the answer. Asset manager demand for the

US dollar has changed more than any other asset class this year. So the

critical question in 2025 turned into “How far will the dollar depreciate?”

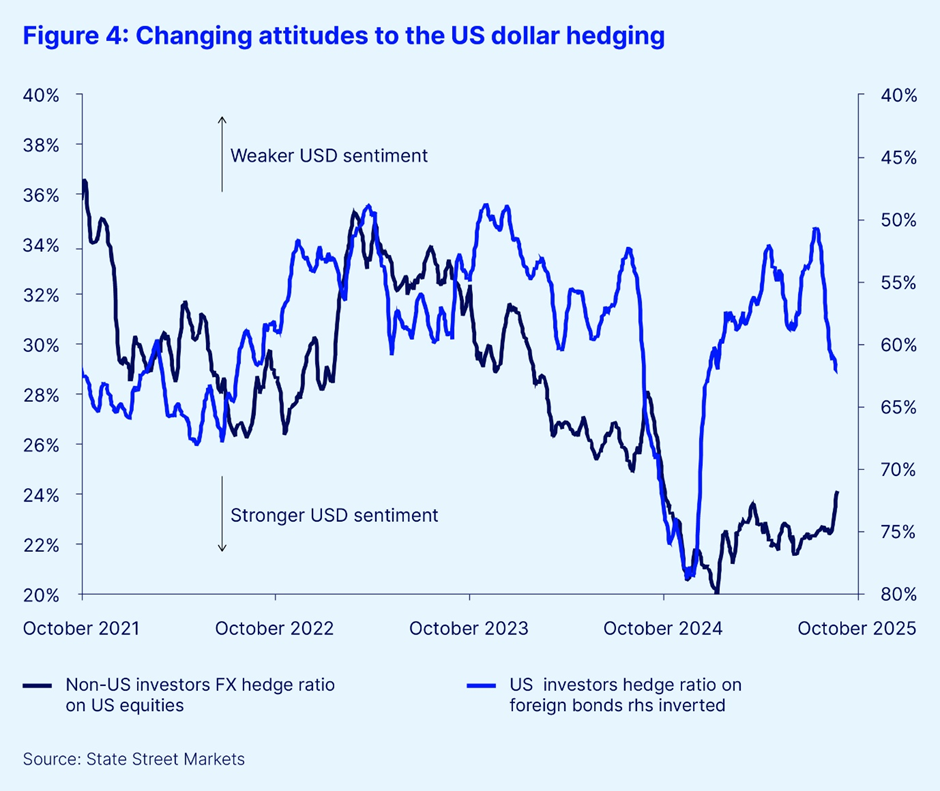

For fixed-income managers based in the US, the fear of a

rapid US dollar appreciation following the US Presidential election manifested

itself in a surge in forward US dollar buying that took their hedge ratio on

their foreign bond holdings to a peak of near 80 percent, a 25-year high. This

ratio peaked in mid-January and as the feared US dollar overshoot failed to

materialize, US managers sold their US dollars forward rapidly to bring their

hedge ratio back down to an unusually low level of 50 percent. That excessive

US dollar pessimism has corrected somewhat in the past six weeks, and hedge

ratios of US managers are now back toward recent averages. This part of the US

dollar unwind would seem therefore to be done (See Figure 4).

However, non-US investors are still playing catch up. Non-US

investor hedge ratios on their US equity holdings have started to rise more

sharply in recent weeks, but are still somewhat below recent averages. This indicates

that for all the exceptional foreign buying of US equities in the past five years,

there have been relatively fewer forward sales of the US dollar to offset the

currency risk. The adjustment is, however, underway.

This will give the US dollar a very different starting point

in 2026. While 2025 began with what turned out to be excessive asset manager optimism

about US dollar strength, 2026 will begin with a good deal of pessimism. This

doesn’t mean there isn’t potential for the US dollar to weaken further. Non-US

managers could still hedge a far higher proportion of their US equity holdings

than they do today. But given expectations for further US dollar weakness are

now somewhat built into investor holdings, the bar for the currency to surprise

on the downside is now much higher. And in contrast to US equities, it has been

the weakness of the US dollar alongside the ongoing change in investor attitude

toward it, that has been exceptional.

Looking back to look forward

The year has been characterized by a major market shift

around the US dollar, a doubling down on US and US tech exceptionalism, as well

as unprecedented policy uncertainty. In our August update of Market

Signals and Shifts, we suggested that “policy uncertainty may, just may,

start to decline.” But that failed to materialize. Since then, concerns about

tariff policy have come and gone, and a US government shutdown is underway —

all alongside policy volatility in Japan and France, amongst others. What has

been consistent this year, apart from a brief period, is the willingness of investors

to look past this uncertainty, even against a backdrop of large and relatively

concentrated overweight positions in equity markets.

This apparent resilience will no doubt form a big part of

the market outlooks that are being penned for 2026. But resilience — even

repeated resilience as in recent years — does not mean markets are invulnerable.

Our Market Outlook for 2026 will feature gauges of market froth to capture the

risk of bubbles across sectors. In particular, we’ll take a closer look at the

credit cycle and US recession risk, a notable acceleration in inflation outside

of the US, and the debate as to whether shifts in investor sentiment around Treasuries

and the US dollar may be more structural than tactical in nature. In short,

2025 has been a terrific confidence boost for markets, but that success, or

perhaps feat, may be harder to repeat in 2026.

Disclaimer & Risk

Author Bios

Michael Metcalfe

Michael is Senior Managing Director and Head of Macro Strategy at State Street Markets

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.