November 7, 2022

Working Papers

Complimentary CONTENT

Measuring Market Froth

By: Rajeev Bhargava, Michael Guidi, Robin Greenwood, Zachary Crowell

November 7, 2022

By: Rajeev Bhargava, Michael Guidi, Robin Greenwood, Zachary Crowell

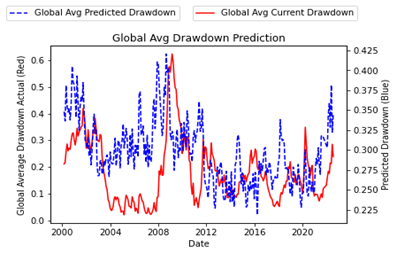

We define equity markets and sectors to be “frothy” when the probability of a future drawdown in prices is high. Using simple panel regressions, we analyze data across 80 countries and 400 country-sectors to identify and evaluate which factors--including issuance, volatility, the price path, and flow-based factors-- are most predictive of future sector-level drawdowns. We translate our predictive model into indicators for sector- and market-level froth.

Author Bios

Rajeev Bhargava

Michael Guidi

Michael Guidi is a member of the Investor Behavior Research team at State Street Associates (SSA). Since joining SSA in 2011, Michael’s research has spanned multiple product lines including our behavioral indicators, media sentiment products, and high-frequency inflation indicators. He holds a Bachelor of Science in electrical and computer engineering from University of Florida, a MS in mathematical finance from Boston University, and the CFA charter.

Robin Greenwood

Robin is a professor at Harvard Business School specializing in behavioral finance, macro market inefficiencies, price bubbles, financial crises, and the role of government and central banks in debt markets. His published articles have garnered six distinguished awards for their impact and originality. Robin’s foundational research on investor behavior and prices offers State Street clients new avenues to understand and apply proprietary indicators of flow and positioning across markets.

Zachary Crowell

Zachary is a quantitative researcher for State Street Associates, focusing on investor behavior research. He holds a BS in Mathematics and a MSc in Applied Mathematics from Northeastern University.

1. Peter L. Bernstein Award for Best Article in an Institutional Investor Journal in 2013; Bernstein-Fabozzi/Jacobs-Levy Award for Outstanding Article in the Journal of Portfolio Management in 2006, 2009, 2011, 2013 (2), 2014, 2015, 2016, 2021; Graham & Dodd Scroll Award for article in the Financial Analysts Journal in 2002 and 2010. Roger F. Murray First Prize for Research Presented at the Q Group Conference in 2012, 2021, 2023. Harry M. Markowitz Award for Best Paper in the Journal of Investment Management in 2022, 2023. Doriot Award for Best Private Equity Research Paper in 2022.